Dealing with the complex Fringe Benefits Tax (FBT) is one of the many financial challenges that regional breeding and racing operations must face. Any relief from this tax is very welcome!

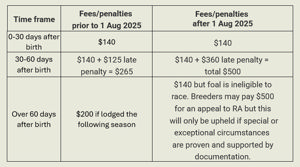

![]()

It is well known that a legitimate exemption from FBT for farm operations that provide car benefits to employees is the “eligible” vehicles concession under the FBT Act. Refer definitions below, noting most of these eligible vehicles are “farm-type’ vehicles.

Often the industry thinks that by merely providing an eligible vehicle to an employee means there is never any FBT implications, the ultimate “get out of FBT jail card.” This article provides a salient reminder that this is not the case. The type and regularity of private use is also a significant factor in gaining this vehicle FBT exemption.

- Vehicles eligible for the exemption

For reference, the following vehicles are eligible for the FBT car exemption:

- a single cab ute

- a dual cab ute that is designed to either

- carry a load of 1 tonne or more

- carry more than 8 passengers (including the driver)

- carry a load of less than 1 tonne but is not designed for the principal purpose of carrying passengers. a panel ute or goods ute

- a modified vehicle (such as a hearse) if, for the entire FBT year when the car is used by the employee, the modification permanently affects the inherent design of the vehicle.

- a taxi

- any 4-wheel drive vehicle that is designed either

- to carry a load of 1 tonne or more

- to carry more than 8 passengers (including the driver)

- for a principal purpose other than carrying passengers, as indicated by its appearance, marketing specification or carrying capacity – for more information see TD 94/19

- any other road vehicle that is designed to carry either

- a load of 1 tonne or more

- more than 8 passengers (including the driver).

- Uses eligible for the exemption

A fringe benefit is an exempt benefit where the private use of an eligible vehicle by a current employee during a fringe benefits tax (FBT) year is limited to work-related travel, and other private use that is ‘minor, infrequent and irregular.’

A 2018 ATO guideline, “PCG 2018/3 FBT: Exempt car benefits — determining private use of vehicles”, notes at paragraph 6 that you can choose to rely on the guideline to avoid the need to keep records about an employee’s private use of an eligible vehicle if:

(a) you provide an eligible vehicle to a current employee

(b) the vehicle is provided to the employee for business use to perform their work duties

(c) the vehicle had a GST-inclusive value less than the luxury car tax threshold at the time the vehicle was acquired

(d) the vehicle is not provided as part of a salary packaging arrangement and the employee cannot elect to receive additional remuneration in lieu of the use of the vehicle

(e) you have a policy in place that limits private use of the vehicle and obtain assurance from your employee that their use is limited to use as outlined in subparagraphs (f) and (g) of this paragraph

(f) your employee uses the vehicle to travel between their home and their place of work and any diversion adds no more than two kilometres to the ordinary length of that trip, and

(g) for journeys undertaken for a wholly private purpose (other than travel between home and place of work), the employee does not use the vehicle to travel

(i) more than 1,000 kilometres in total, and

(ii) a return journey that exceeds 200 kilometres.

Of particular importance is implementing a policy that complies with para (e) above and obtaining suitable assurance from the employee that they have complied with the requirements of the Guidelines. Best practice would be to ensure that both matters are documented so that they can be readily produced to the ATO if required.

If any of the above criteria (numbered (a) through to (g)) were not satisfied, e.g. the vehicle had a GST-inclusive value greater than the luxury car tax threshold, then the employer is unable to rely upon the concessional treatment in PCG 2018/3. Instead, such an employer will have to self-assess if the private use of the vehicle (other than home to work travel) is strictly minor, infrequent and irregular to claim the FBT exemption.

- The ATO’s compliance approach

If you do rely on this guideline, it’s important to note that you do not need to keep records about your employee’s use of the vehicle that demonstrate that the private use of the vehicle is ‘minor, infrequent and irregular’ and the ATO will not devote compliance resources to review that you can access the car-related exemptions for that employee.

- ATO example – diversion and wholly private travel

To help you understand how this FBT exemption applies for eligible vehicles, I will slightly modify an example from the PCG 2018/3 guideline.

A Hunter Valley stud employer provides an employee with a new dual cab ute designed to carry a load of 1 tonne or more. The ute is provided to the employee to enable the employee to carry bulky equipment to and from their work sites. The ute is not provided as part of a salary packaging arrangement, and was acquired for a value below the applicable luxury car tax threshold.

The ute is an eligible vehicle. The ute is garaged at the employee’s home and the employee uses the ute to travel between their home and their place of employment. The employer has a strict policy in place about limiting the private use of the vehicle.

The employee usually stops at the newsagent to pick up a newspaper on their way to work. The diversion adds no more than two kilometres to the total trip from home to work.

On 10 occasions during the FBT year, the employee also transported their niece to school in the ute during the employee’s journey from home to work. The journeys from home to work generally do not exceed 20 kilometres.

At the end of the 2025 FBT year, the employer receives an email from the employee. The email outlines that multiple journeys were undertaken in the FBT year for a wholly private purpose and these journeys did not exceed 1,000 kilometres in total. The employee also outlines in the email that in driving to and from work, no diversions were undertaken that exceeded two kilometres. The employer is satisfied that the employee has adhered to their policy about limited private use.

The employer is able to rely on this Guideline as the requirements in paragraph 6 of this Guideline are met.

Prepared by:

PAUL CARRAZZO CA, CPA

Partner - Baumgartners

1/35 Cotham Rd, Kew, VIC, 3101

TEL: +61 3 9851 9000

MOB: 0417 549 347

E-mail: p.carrazzo@baumgartners.com.au